Dubai is one of the world's premier financial centres and navigating its banking and finance legal landscape requires specialist expertise, not generalist advice.Whether you are a financial institution managing regulatory obligations under the UAE Central Bank, a business structuring a complex loan facility, an investor dealing with a banking dispute, or an individual facing debt recovery action, Al Adl Legal's banking and finance lawyers in Dubai provide the expert legal counsel you need.

Our banking and finance legal practice is built around the full spectrum of UAE financial law fromregulatory compliance and transactional advisorytobanking dispute litigation and Islamic finance structuring. We advise clients under the UAE's federal banking framework, the Dubai Financial Services Authority (DFSA) regulatory regime within the DIFC, and the Abu Dhabi Global Market (ADGM) Financial Services Regulatory Authority (FSRA). With the enactment ofFederal Decree-Law No. 6 of 2025 on the Regulation of Financial Institutions and Activitiesthe most significant overhaul of UAE banking law in decades having specialist legal counsel is more critical than ever.

Understanding which regulatory body governs your banking or financial matter is the essential starting point for any legal strategy in the UAE. The Regulation is divided between federal regulations and free zone regimes with significant differences in rules, enforcement, and dispute forums.

Regulator / Body | Jurisdiction | What It Governs |

UAE Central Bank (CBUAE) | UAE Mainland (all emirates) | Licensing of banks, finance companies & payment institutions. Consumer protection. AML/CFT oversight. Wage Protection System. Governed by Federal Decree-Law No. 6 of 2025. |

Dubai Financial Services Authority (DFSA) | DIFC (Dubai International Financial Centre) | Regulates financial services firms operating within DIFC. Applies the DFSA Rulebook under a common law framework based on English law. |

Securities & Commodities Authority (SCA) | UAE Mainland | Capital markets, investment funds, securities regulation, listed companies, and commodities trading. |

Virtual Assets Regulatory Authority (VARA) | Dubai (mainland & DIFC) | UAE's first dedicated virtual assets regulator. Licenses and supervises crypto exchanges, digital asset service providers, and DeFi platforms. |

Financial Services Regulatory Authority (FSRA) | ADGM (Abu Dhabi Global Market) | Regulates financial services within ADGM. Common law jurisdiction with its own employment, commercial and financial regulatory framework. |

UAE Insurance Authority | UAE Mainland | Regulates conventional and Takaful (Islamic) insurance companies and products. |

Key 2025 Update: Federal Decree-Law No. 6 of 2025 on the Central Bank, Regulation of Financial Institutions and Activities (effective September 2025) replaces the previous Central Bank Law and significantly expands CBUAE supervisory powers, introduces new licensing categories for fintech and digital payment providers, and strengthens AML/CFT enforcement. All UAE financial institutions must review their compliance frameworks against this new law.

Al Adl Legal provides comprehensive banking and finance legal services for financial institutions, corporations, and individuals across the UAE. Each service area below is handled by lawyers with specialist knowledge of UAE banking regulation, DIFC/ADGM financial law, and Islamic finance principles.

Banking Regulatory Compliance & Licensing

The UAE's banking regulatory environment is one of the most comprehensive in the region and one of the fastest-changing. Following the enactment of Federal Decree-Law No. 6 of 2025, financial institutions face new licensing obligations, expanded reporting requirements, and enhanced consumer protection duties. Al Adl's banking lawyers advise financial institutions, fintech companies, payment service providers, and digital asset businesses on their regulatory obligations from initial licensing through ongoing compliance.

• Licensing applications to the UAE Central Bank (CBUAE) for banks, finance companies, and payment institutions

• DFSA regulatory compliance advisory for DIFC-licensed financial services firms

• FSRA regulatory advisory for ADGM-based financial institutions

• VARA licensing and compliance for virtual asset service providers and crypto exchanges

• AML/CFT policy drafting, compliance programme design, and regulatory gap analysis

• KYC framework review and CBUAE reporting obligation advisory

• Consumer protection compliance under CBUAE guidelines and Federal Decree-Law No. 6/2025

• Regulatory correspondence and liaison with CBUAE, DFSA, SCA, and VARA on behalf of clients

Loan Agreements, Finance Transactions & Transactional Advisory

Structuring and documenting banking and finance transactions in the UAE requires expert knowledge of both UAE civil law and, for DIFC/ADGM transactions, common law principles. A poorly drafted loan agreement, one that fails to properly address security, default triggers, or Sharia compliance requirements, can render an entire financing unenforceable. Al Adl's finance lawyers in Dubai draft, review, and negotiate all categories of finance documentation for lenders, borrowers, and sponsors.

• Drafting and negotiating loan agreements, credit facility agreements, and syndicated finance documentation

• Project finance structuring for real estate, infrastructure, energy, and development projects

• Trade finance and letters of credit - documentation and dispute advisory

• Acquisition finance and leveraged buyout financing documentation

• Asset-backed finance, mortgage security, and pledge documentation

• Reviewing and advising on guarantees, security packages, and inter-creditor arrangements

• Debt restructuring and refinancing - renegotiating terms, standstill agreements, waiver letters

• Fintech lending documentation and regulatory compliance for digital lending platforms

Banking Dispute Resolution & Litigation

When a banking dispute reaches litigation, the choice of forum UAE Courts, DIFC Courts, or arbitration is a critical strategic decision that must be made correctly from the outset. DIFC Courts apply English common law; UAE Courts operate in Arabic under civil law and Islamic principles; arbitration offers confidentiality and enforcement advantages under the New York Convention. Al Adl's banking dispute lawyers have represented financial institutions, corporations, and individuals in all three forums.

• Representing banks and financial institutions in loan recovery litigation before UAE Courts

• Defending borrowers against enforcement proceedings and asset freezing orders

• Banking dispute representation before the DIFC Courts (Small Claims Tribunal and Urgent Applications)

• Cheque dispute litigation - including bounced cheques and post-2022 decriminalisation cases

• Credit card disputes, merchant disputes, and banking fraud claims

• Asset recovery and judgment enforcement - domestically and internationally

• Representing clients in DIAC and ICC arbitration proceedings involving banking disputes

• Challenging unlawful bank account freezing, asset seizure, and travel bans

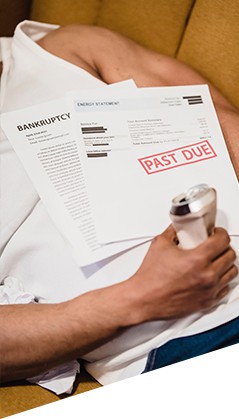

Debt Recovery for Financial Institutions & Businesses

Debt recovery in the UAE follows a structured legal process and the speed of recovery depends heavily on the quality of documentation, the correct choice of legal forum, and the experience of the lawyers executing the process. Al Adl's debt recovery lawyers in Dubai represent banks, financial institutions, and businesses pursuing outstanding debts across all categories from personal loan defaults and corporate credit facilities to trade receivables and bounced cheques.

• Issuing formal demand letters and legal notices to defaulting borrowers

• Filing debt recovery claims before the UAE Courts of First Instance

• Applying for precautionary attachment orders to freeze debtor assets before judgment

• Representing creditors in DIFC Court Small Claims proceedings (claims up to USD 200,000)

• Enforcement of UAE court judgments - execution proceedings and bank attachment orders

• Enforcement of foreign court judgments and arbitral awards in UAE

• Corporate debt restructuring negotiation on behalf of creditors

• Recovery of debts from companies in liquidation or insolvency proceedings

Islamic Banking & Finance Law - Sharia-Compliant Transactions

The UAE is one of the world's leading centres for Islamic finance. Sharia-compliant banking products are governed by principles that fundamentally differ from conventional finance prohibiting interest (riba), excessive uncertainty (gharar), and speculative activity (maysir). Al Adl's Islamic finance lawyers advise banks, investors, and businesses on structuring, documenting, and managing Sharia-compliant financial transactions in compliance with both UAE law and Islamic principles.

• Structuring and documenting Murabaha (cost-plus-profit) financing transactions

• Ijara (lease finance) documentation for real estate and asset finance

• Musharakah (partnership finance) and Diminishing Musharakah agreements

• Sukuk (Islamic bond) issuance structuring, documentation, and regulatory filing

• Mudarabah (profit-sharing) investment structures for Islamic funds

• Takaful (Islamic insurance) product compliance and advisory

• Sharia compliance review for existing financial products and agreements

• Advisory on UAE Central Bank's Islamic finance regulatory framework and AAOIFI standards

AML, KYC & Financial Crime Compliance

Anti-money laundering (AML) and counter-terrorism financing (CFT) compliance is one of the highest-risk areas for UAE financial institutions. The Central Bank of the UAE, the DFSA, and the Financial Intelligence Unit (FIU) all impose strict obligations. Non-compliance can result in licence suspension, regulatory fines of up to AED 100 million, and personal liability for senior management. Al Adl's AML compliance lawyers help financial institutions design, implement, and defend their compliance programmes.

• AML/CFT compliance framework design and implementation under Federal Decree-Law No. 6/2025

• KYC policy review and customer due diligence (CDD) programme advisory

• Responding to CBUAE AML investigations and enforcement actions

• Suspicious transaction report (STR) advisory, when and how to file with the UAE FIU

• Representing financial institutions in regulatory proceedings before CBUAE and DFSA

• Training senior management and compliance teams on UAE AML obligations

• VARA virtual asset AML compliance for cryptocurrency and digital asset service providers

• Sanctions compliance - UAE, OFAC, EU, and UN sanctions screening advisory

Fintech & Digital Finance Legal Advisory

Dubai has positioned itself as a global fintech hub through the establishment of DIFC Fintech Hive, the VARA virtual assets regulatory framework, and the UAE Central Bank's Open Finance framework. For fintech startups, digital lenders, payment platforms, crypto exchanges, and digital banks, navigating this rapidly evolving regulatory landscape requires specialist legal counsel. Al Adl advises fintech businesses from initial incorporation and licensing through product launch and ongoing regulatory compliance.

• CBUAE licensing for digital banks, payment institutions, and stored-value facility providers

• DFSA's Innovation Testing Licence (ITL) application advisory for DIFC fintech firms

• VARA licensing for virtual asset service providers (VASPs) - Category 1, 2, 3, 4 licences

• Open Finance and Open Banking regulatory compliance under CBUAE framework

• Regulatory advisory for Buy Now Pay Later (BNPL) providers in the UAE

• Blockchain and smart contract legal advisory and documentation

• Cryptocurrency and digital asset dispute resolution and regulatory defence

• Fintech partnership and third-party service provider agreement structuring

The UAE is one of the world's largest Islamic finance markets, with over USD 900 billion in Sharia-compliant assets under management. Understanding the core Islamic finance products is essential for any business operating in the UAE financial sector.

Murabaha مرابحة | Cost-plus-profit financing. The bank purchases an asset and sells it to the client at a higher price payable in instalments. No interest is charged, profit is built into the purchase price. The most common Islamic finance product in the UAE. |

Ijara إجارة | Islamic lease finance. The bank buys an asset and leases it to the client for an agreed period and rental. At the end of the term, ownership may transfer to the client (Ijara wa Iqtina). Used extensively in real estate and equipment finance. |

Musharakah مشاركة | Partnership finance. Bank and client jointly invest in a project or asset and share profits and losses in proportion to their investment. Diminishing Musharakah is the most common form used in home financing. |

Sukuk صكوك | Islamic bonds (certificates of investment). Sukuk represent ownership of a tangible asset, usufruct, or investment project — not a debt obligation. UAE is one of the world's largest Sukuk issuance markets. |

Mudarabah مضاربة | Profit-sharing arrangement. One party provides capital (Rab-ul-Maal); the other provides labour/expertise (Mudarib). Profits are shared per agreed ratio; losses borne solely by the capital provider (unless due to negligence). |

Takaful تكافل | Islamic insurance based on mutual solidarity and shared risk, not conventional premium/indemnity structure. Participants contribute to a pool and share risks collectively. Sharia-compliant alternative to conventional insurance. |

Wakalah وكالة | Agency contract. The bank acts as agent (Wakeel) for the client to invest funds on their behalf for a fixed fee. Common in Islamic investment deposits and Sukuk structures. |

Clients operating within the Dubai International Financial Centre (DIFC) are subject to a fundamentally different legal regime from the UAE mainland. Choosing the wrong legal forum or misunderstanding which law governs your contract can be fatal to a banking claim.

Factor | DIFC (DFSA regulated) | UAE Mainland (CBUAE regulated) |

Governing law | DIFC Law - based on English common law | UAE Federal Law - civil law + Islamic principles |

Dispute forum | DIFC Courts (English language proceedings) | UAE Courts (Arabic proceedings) → Court of First Instance |

Banking regulator | Dubai Financial Services Authority (DFSA) | UAE Central Bank (CBUAE) — Federal Decree-Law No. 6/2025 |

Interest/riba | Conventional interest permissible | Islamic finance products widely used; riba restrictions apply to Islamic banks |

Security enforcement | DIFC Court enforcement - fast track available | UAE Court attachment orders and execution proceedings |

Arbitration | ICC, LCIA, DIAC, DIFC-LCIA - all available | DIAC, ICC - common, must specify in contract |

AML framework | DFSA AML Rulebook (module 8) | CBUAE AML/CFT Guidelines + Federal Decree-Law No. 20/2018 |

Fintech licensing | DFSA Innovation Testing Licence + Fintech Hive | CBUAE regulatory sandbox + VARA (virtual assets) |

Many DIFC financial services agreements contain a jurisdiction clause specifying DIFC Courts. If you receive a claim in the DIFC Courts, you have a limited window to challenge jurisdiction. Engage a banking lawyer immediately, missing the jurisdictional challenge deadline can result in proceedings continuing in a forum you did not intend.

Step 1: Legal Notice | Formal written demand sent to the debtor specifying the amount owed, the legal basis for the claim, and a deadline for payment (typically 7-14 days). This is a mandatory first step and preserves your legal position. |

Step 2: Precautionary Attachment | Before filing a court case, you may apply for a precautionary attachment (freezing order) on the debtor's bank accounts and assets. Requires demonstrating that the debt is established and there is a risk the debtor will dissipate assets. |

Step 3: Court Filing | File the debt claim before the Court of First Instance (for amounts above AED 50,000). The court issues a summons to the debtor. Al Adl prepares the Statement of Claim with all supporting documentation. |

Step 4: Court Hearing | Both parties appear before the judge. Al Adl presents the debt documentation: loan agreement, payment records, correspondence, and any security. The judge may request additional submissions. |

Step 5: Judgment | The court issues a judgment ordering payment. Timeline: typically 2–4 months for straightforward debt cases. More complex matters (disputed amounts, set-off claims) can take 6–12 months. |

Step 6: Execution | If the debtor does not pay voluntarily, an execution order is obtained. This enables attachment of the debtor's bank accounts, movable property, and real estate, enforceable immediately across the UAE. |

DIFC Track | For DIFC-governed debts, the DIFC Court Small Claims Tribunal handles disputes up to USD 200,000 proceedings in English, with faster timelines (typically 6–8 weeks to judgment). Al Adl represents clients before the DIFC Courts. |

Bounced Cheques | Post-2022 reform: bounced cheques are now primarily a civil matter for first-time offenders. Criminal proceedings still available for intentional fraud. Al Adl advises on the optimal enforcement strategy for your specific cheque dispute. |

Choosing the right banking and finance lawyers in Dubai means choosing a team that combines specialist financial law knowledge with proven litigation capability, and understands both the UAE mainland legal system and the DIFC's common law environment.

UAE Ministry of Justice Licensed Advocates:All Al Adl lawyers hold full practising certificates with rights of audience before UAE Courts, Court of Appeal, Court of Cassation, and DIFC Courts. |

Specialist Banking & Finance Practice:Banking and finance law is a primary practice area at Al Adl, not an add-on. Our lawyers handle banking regulatory, transactional, and dispute matters daily. |

Islamic Finance Expertise:We advise on the full spectrum of Sharia-compliant financial products: Murabaha, Ijara, Musharakah, Sukuk, Mudarabah, and Takaful in compliance with UAE Central Bank Islamic finance guidelines and AAOIFI standards. |

DIFC Court Experience:We represent clients in the DIFC Courts (Civil, Commercial, and Small Claims divisions) under English common law and a specialist capability that many generalist Dubai law firms do not possess. |

Regulatory Knowledge:We track UAE Central Bank regulatory updates, DFSA rulebook changes, VARA virtual asset regulations, and SCA capital markets guidance in real time. Your advice will always reflect the current legal position. |

Confidentiality:Banking and financial matters require absolute discretion. All client matters are protected by legal professional privilege. Your financial information is never disclosed. |

Multilingual:Arabic-English bilingual team. We conduct UAE Court proceedings in Arabic and DIFC proceedings in English. Additional language support available for Urdu, Hindi, and French. |

Business Bay, Dubai:Located centrally near DIFC, the UAE Courts complex, CBUAE offices, and Dubai's main financial district. Minutes from the heart of Dubai's banking sector. |

Free First Consultation:We offer a free, no-obligation initial consultation for all banking and finance legal matters. Understand your legal position and options before committing to anything. |

Banking lawyers in Dubai advise financial institutions, corporations, and individuals on the full spectrum of banking and financial legal matters including regulatory compliance, loan agreement drafting and negotiation, banking dispute resolution and litigation, debt recovery, Islamic finance structuring, AML/KYC compliance, and DIFC/DFSA regulatory advisory. Al Adl's banking lawyers handle both transactional advisory (helping you structure and document deals) and contentious matters (representing you in court or arbitration when disputes arise).

Step 1: File a formal written complaint directly with the bank's Customer Complaints department. Step 2: If unresolved within 30 days, escalate to the Central Bank of the UAE Consumer Protection Department via their online portal (cbuae.gov.ae). Step 3: If your account is with a DIFC-regulated bank, complaints go to the DFSA. Step 4: If informal channels fail, a banking lawyer can file a court claim before the UAE Courts or DIFC Courts depending on which institution governs your bank. Al Adl handles banking complaint escalations and dispute litigation for individuals and businesses.

Islamic banking operates under Sharia law principles primarily the prohibition of interest (riba), excessive uncertainty (gharar), and speculative activity (maysir). Instead of charging interest, Islamic banks use profit-sharing arrangements (Mudarabah), cost-plus-profit sales (Murabaha), lease financing (Ijara), and partnership structures (Musharakah). The UAE has one of the world's most developed Islamic finance markets, with major UAE banks (Emirates Islamic, Abu Dhabi Islamic Bank, Dubai Islamic Bank) operating fully Sharia-compliant. Al Adl advises on the structuring and compliance of all Islamic finance products.

The debt recovery process in Dubai involves: (1) Sending a formal legal demand letter giving the debtor a deadline to pay. (2) Applying for a precautionary attachment (freezing order) on the debtor's assets if there is a risk of dissipation. (3) Filing a claim before the UAE Court of First Instance (for claims above AED 50,000) or the DIFC Small Claims Tribunal (for DIFC-governed debts up to USD 200,000). (4) Obtaining a judgment and enforcing it through attachment of bank accounts and property. Al Adl manages the entire debt recovery process, from legal notice through to enforcement execution.

Following the 2022 reforms to the UAE Penal Code, the legal consequences of a bounced cheque depend on intent and history. For a first-time bounced cheque without fraudulent intent, it is primarily a civil matter the payee files a civil claim for the cheque amount. Criminal proceedings remain available for intentional fraud (deliberately issuing a cheque knowing funds are insufficient). Banks may also exercise their right to report the matter to the Central Bank, which can impact the issuer's credit and banking access. Al Adl advises both creditors seeking to enforce cheques and individuals/businesses defending against bounced cheque claims.

The Dubai Financial Services Authority (DFSA) is the independent financial regulator for the Dubai International Financial Centre (DIFC). It regulates: banks and financial institutions based in DIFC, insurance companies, investment firms, collective investment funds, Islamic finance firms operating within DIFC, and fintech companies with a DFSA Innovation Testing Licence. If your business is incorporated in the DIFC and provides financial services, you must hold a DFSA licence. Al Adl advises on DFSA licensing applications, ongoing compliance, and regulatory enforcement defence.

Federal Decree-Law No. 6 of 2025 on the Central Bank, Regulation of Financial Institutions and Activities came into force on 16 September 2025 replacing the previous Central Bank Law that had governed UAE banking since 2018. Key changes include: expanded CBUAE supervisory powers over fintech and digital payment providers, new licensing categories for buy-now-pay-later platforms and open banking providers, strengthened AML/CFT enforcement with higher penalties, enhanced consumer protection requirements for financial institutions, and new governance obligations for senior management. Every UAE-licensed financial institution needs to review its compliance framework against this new law.

Yes. Al Adl's banking and finance lawyers are qualified to practice before UAE federal courts (Court of First Instance, Court of Appeal, Court of Cassation) and before the DIFC Courts (civil, commercial, and Small Claims divisions). This dual-court capability is important because the legal framework, language, and enforcement mechanisms differ significantly between the two jurisdictions. We assess your matter and advise on the optimal forum including whether an arbitration clause in your contract overrides both court options.

AML/CFT non-compliance penalties in the UAE are among the most severe in the region. Under the UAE AML Law and Federal Decree-Law No. 6/2025: financial institutions face fines of up to AED 100 million for serious violations. Licences can be suspended or revoked. Senior management individuals face personal fines of up to AED 5 million and criminal prosecution. The UAE FIU (Financial Intelligence Unit) also reports to FATF meaning non-compliance can affect a firm's international banking relationships. Al Adl helps financial institutions design robust compliance programmes and defend against regulatory enforcement action.

Our team of highly-skilled and experienced lawyers specialize in a variety of areas of practice. With a comprehensive knowledge of UAE legislation, we are well-equipped to provide strategic counsel and effective solutions.

We prioritise our clients' interests and strive to deliver personalised legal solutions. We take the time to thoroughly understand your unique situation, objectives, and concerns. By developing a close working relationship with you, we can provide sound advice and guidance.

Our dedication to excellence sets us apart. We are committed to delivering exceptional legal services, consistently meeting and exceeding our clients' expectations. With meticulous attention to detail, thorough research, and diligent case preparation, we leave no stone unturned.

We uphold the highest standards of integrity and professionalism in all our interactions. We understand the sensitive nature of legal matters and the importance of confidentiality. Rest assured that your information will be handled with the utmost discretion and respect.

Clients

AED Recovered

Countries

Success Rate